State of Africa's Infrastructure Report 2026

The Africa We Build: From Capital to Systems. Deploying Infrastructure for Industrialisation, Integration, and Resilience.

After two years of establishing the State of Africa’s Infrastructure Report as a credible, investor-focused reference, the 2026 edition marks a deliberate shift from analysing infrastructure as isolated asset classes to examining it as integrated ecosystems that drive economic transformation.

This shift is not theoretical. A new wave of global shocks – more severe and more unpredictable than those of the past decade, particularly across energy and supply chains – has reinforced a central reality: Africa’s vulnerability lies in the fragmentation and underdevelopment of the systems required to translate resource abundance into resilient, stable and scalable growth.

With a new ecosystem lens, this year’s report reframes each sector: capital through the financial architecture required to mobilise savings and channel them into the real economy; energy through the rewiring of power systems beyond capacity toward flexibility, integration and storage; transport & logistics through trade corridors that maximise network value rather than standalone assets; industry & manufacturing through value-addition and resilient supply chains in strategic sectors such as fertilizers, refining, metals and food systems; and digital infrastructure through ecosystems that enable productivity, innovation and digitally-driven growth.

Press release

Our Key Findings

Capital

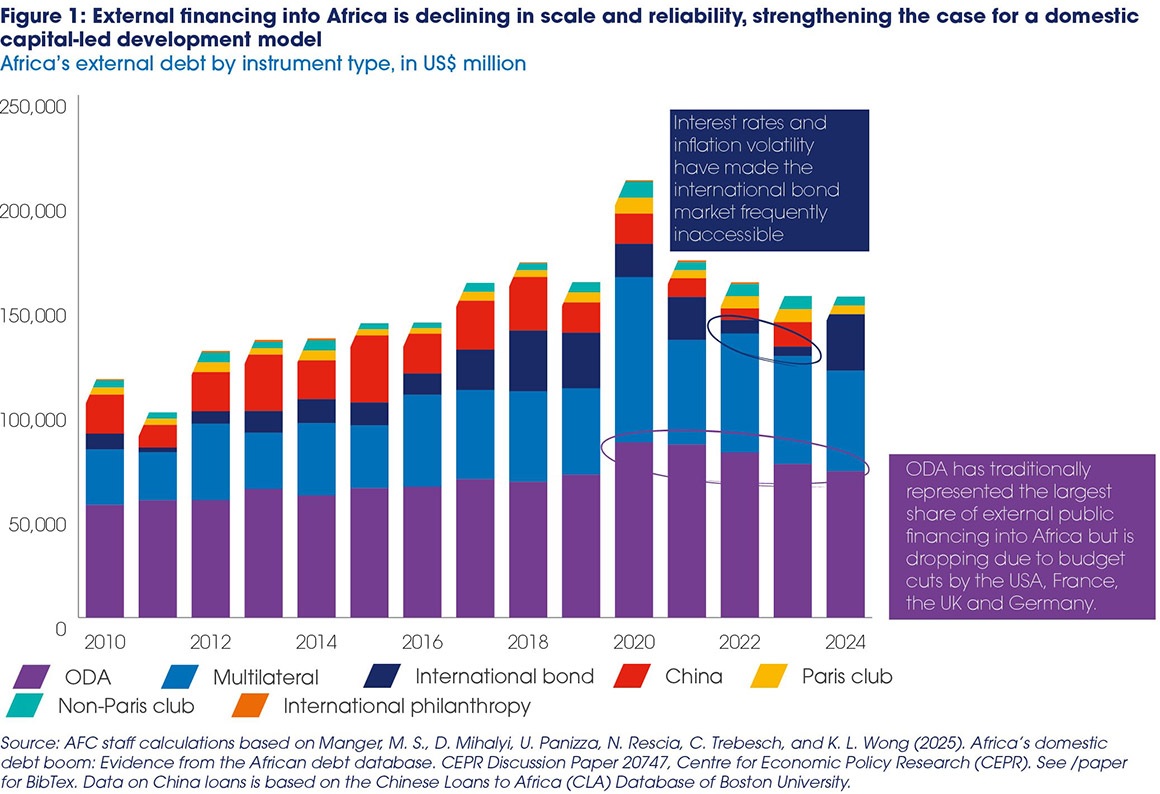

Africa’s constraint is no longer capital mobilisation, but capital deployment. The State of Africa’s Infrastructure Report 2025 established a central conclusion: Africa is not capital-scarce. This year’s report advances that insight. If 2025 demonstrated that capital exists, 2026 focuses on the systems required to deploy it at scale.

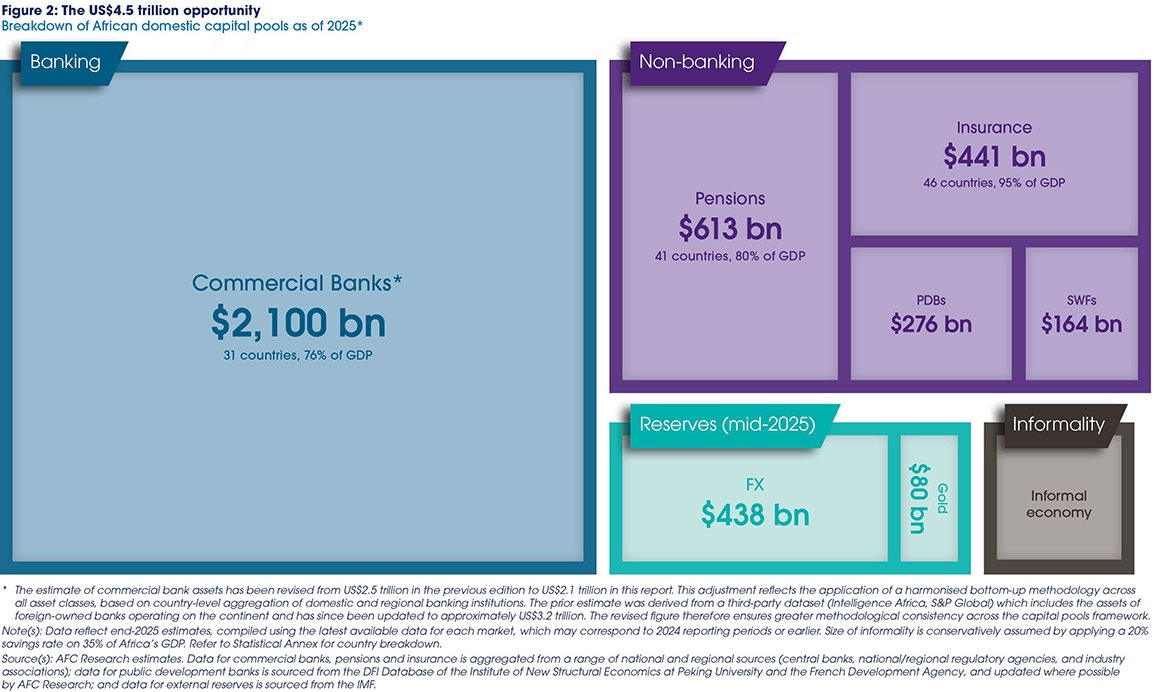

- External financing is retreating and domestic capital must step up. ODA fell by 23.1% in 2025, the largest contraction on record, while Africa’s capital pools now exceed US$4 trillion, including over US$1 trillion in pension and life assets, highlighting the growing potential of non-bank institutional capital.

- Domestic debt markets have scaled but remain structurally shallow. Domestic debt issuance has surged over the past decade, driven largely by short-term bills, resulting in high nominal yields but negative real returns in high-inflation environments—pointing to the need for longer-term instruments and greater real-economy allocation.

- Regulatory frameworks for pension investments are evolving, but capital remains under deployed. While diversification limits are being relaxed, utilisation remains low—requiring stronger intermediation, credit enhancement and risk-sharing tools to crowd in both domestic and global institutional investors.

- Africa’s demographic window creates a time-bound opportunity. With over 40% of global working-age population growth to 2050 and limited aging pressures before after mid-century, the priority is to convert economic activity into formal savings—leveraging digital public infrastructure (DPI) and mobile money to build long-term capital pools.

Transport & Logistics

The next phase of Africa’s transport networks expansion lies in the operationalization of corridors as supply chains. Reducing transit times, streamlining border processes, and improving multimodal integration can unlock significant gains in trade competitiveness and intra-African commerce without requiring entirely new infrastructure networks.

- The AFC Transport & Logistics Corridors Map shows that a core network of ports, railways and road corridors already spans the continent, linking production zones to regional and global markets. The opportunity now is not to build from scratch, but to make these corridors function as integrated, high-performing systems.This requires operationalising one-stop border posts (OSBPs), improving corridor infrastructure and weighbridge efficiency, and institutionalising corridors through functioning authorities that align public and private stakeholders.

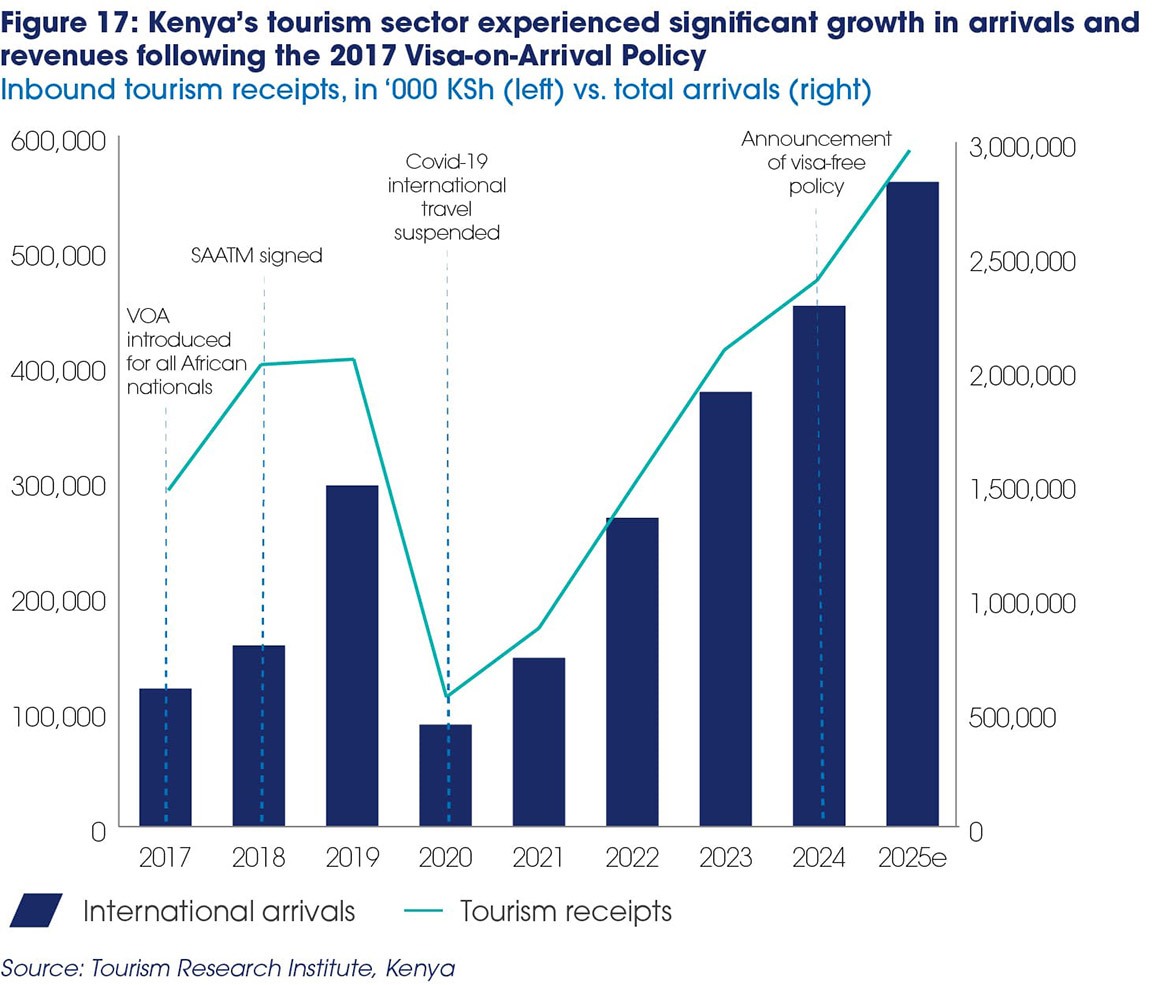

- Aviation provides the fastest layer of integration and must be treated as a core pillar of AfCFTA implementation. Strengthening air connectivity—particularly through cargo infrastructure and full implementation of the Single African Air Transport Market—can accelerate the movement of time-sensitive goods, reduce costs, and connect fragmented markets more rapidly.

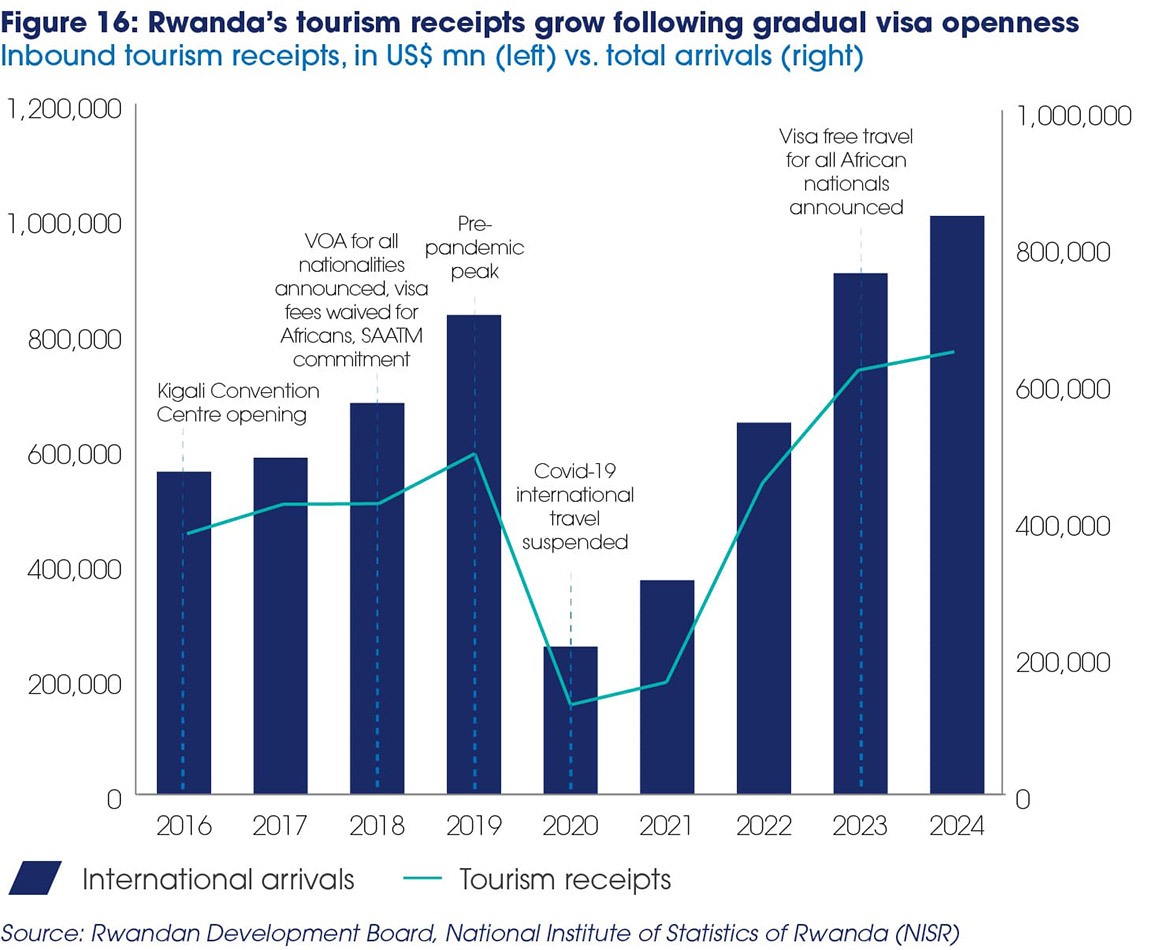

- Where aviation ecosystems are developed, the gains are substantial. Rwanda, Kenya, and Ethiopia illustrate what is achievable when aviation is embedded within a broader economic strategy, combining liberalisation, visa openness, infrastructure investment and effective national carriers to drive tourism, trade, and connectivity. These three models demonstrate the scale of impact, with aviation contributing a combined US$5.5 billion to GDP across these countries and supporting around one million jobs.

- Recent shocks have shown that without storage, buffers and efficient distribution systems, gains in transport efficiency do not translate into lower costs or greater stability. This gap is acute: no African country meets the IEA’s 90-day emergency oil stock requirement, while food storage capacity across the continent covers less than 30% of annual production. Expanding storage capacity, building strategic reserves, and integrating rail and pipeline infrastructure into supply chains are therefore critical to reducing vulnerability in both food and fuel systems.

Energy

Expanding demand from industry, urbanisation, and regional trade creates a clear pathway for scaling African energy systems as a foundation for economic transformation.

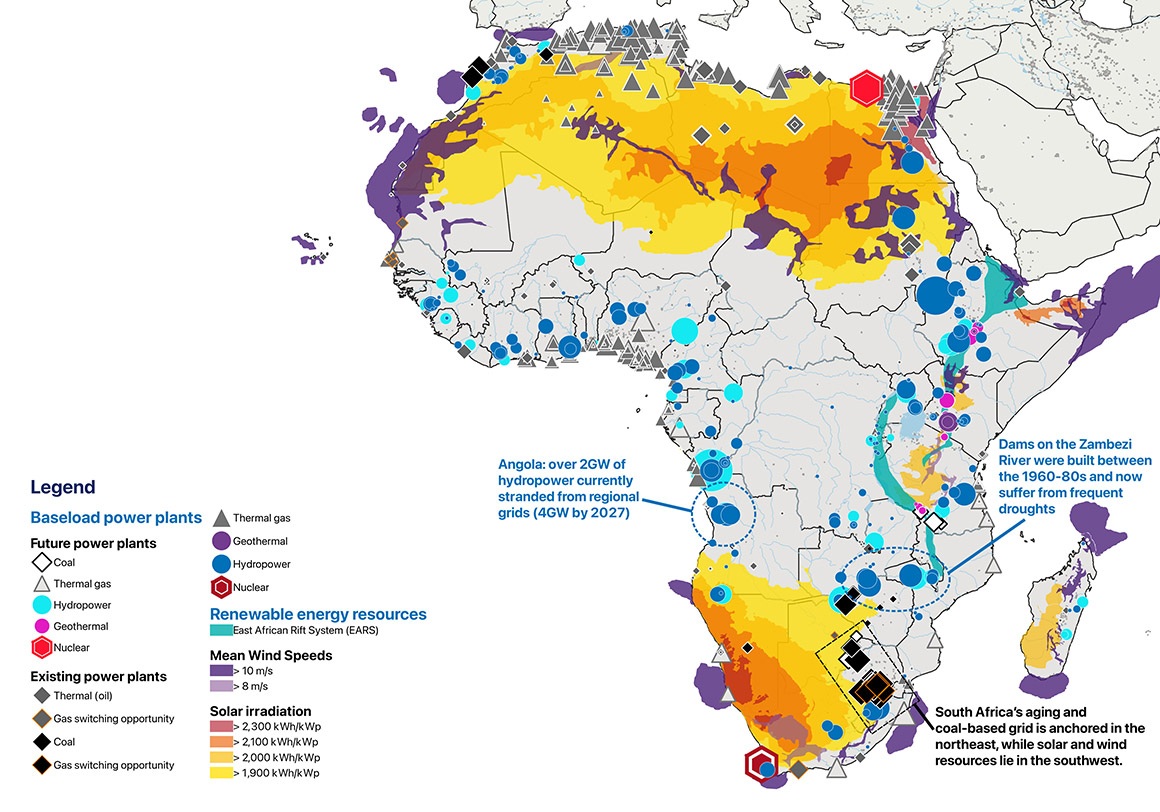

- Africa’s energy systems can become the foundation of industrial growth only if built as integrated systems. The priority is no longer just adding generation capacity, but connecting generation, transmission, storage, fuels, and industrial demand into coherent energy ecosystems that can support large-scale production.

- Transmission must be opened to private capital to unlock system performance. The first Independent Transmission Project (ITP) reaching financial close in 2026 demonstrates that the model works; scaling it will require leveraging markets with strong IPP track records—particularly in East and Southeastern Africa—to crowd in private investment and accelerate grid expansion.

- Regional integration is the fastest pathway to scale, efficiency, and reliability. Bridging power pools through priority interconnectors can unlock stranded capacity in countries such as Angola, Ethiopia, and Uganda, while addressing deficits in major demand centres across the Copperbelt and Southern Africa, turning fragmented national systems into competitive regional energy markets.

- Energy security has become a core economic imperative in a fragmented global system. The 2026 Strait of Hormuz crisis underscores that dependence on imported fuels is a structural vulnerability: refining, storage, and fuel logistics infrastructure are now as critical as electricity systems to economic resilience.

Value additions

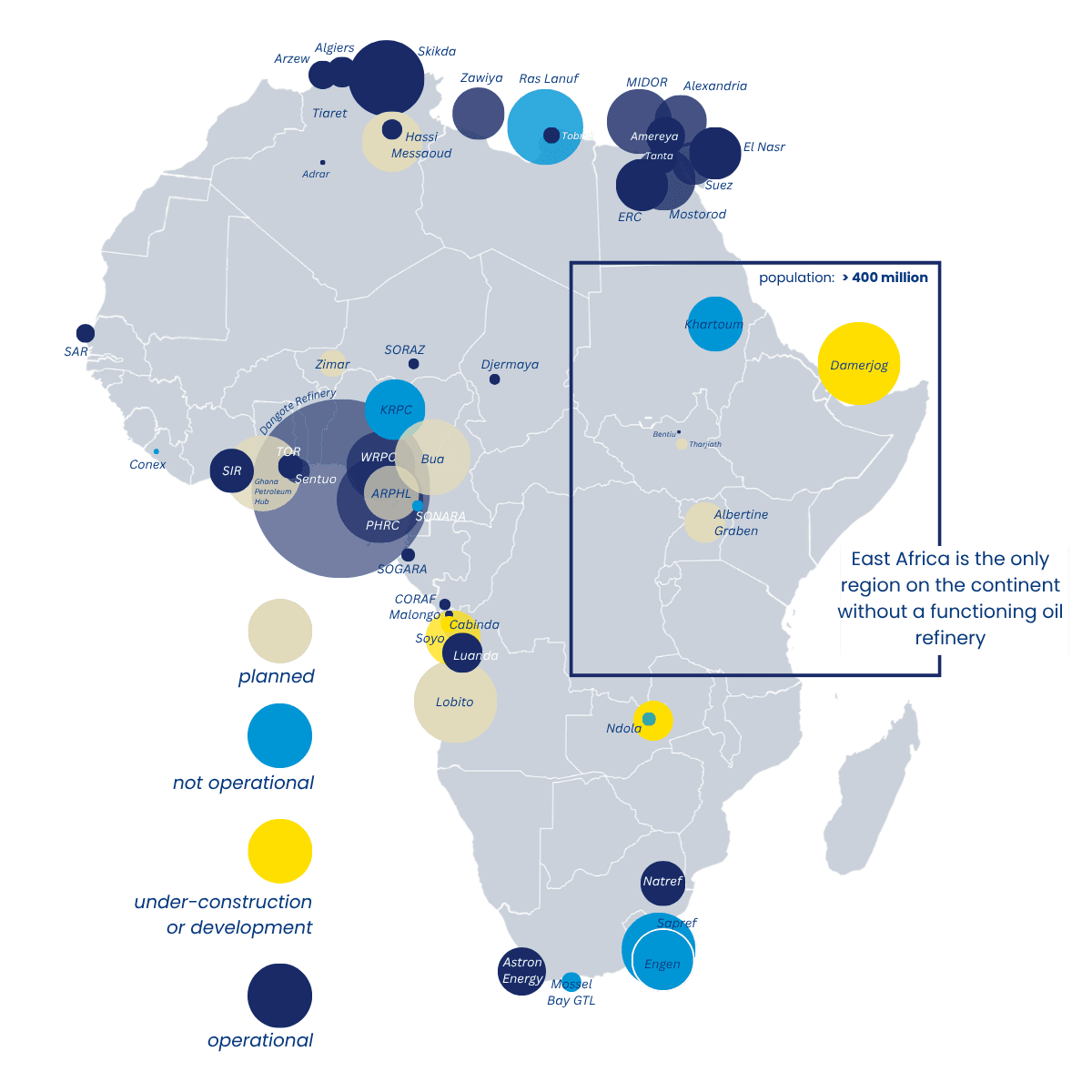

In light of repeated external and geopolitical shocks, Africa's infrastructure gap has become a resilience gap. An import basket of US$230 bn on basic products like fuel, food, plastics, steel and fertilizer means Africa has no shock absorption capacity and keeps importing inflation and exporting jobs since these products are often fabricated from its own resources.

- Fragmented value chains represent a scalable industrial opportunity. The geographic separation of production, processing, and demand is the basis for building integrated regional systems that capture value within the continent. Africa's strategic minerals position illustrates it best: with one of the world's largest endowments of iron ore, bauxite, critical minerals, and inputs to battery and energy systems, the continent has a unique opportunity to anchor global and regional value chains.

- Building on previous reports, our Demand, Resources, Infrastructure and Policy (DRIP) framework highlights key opportunities to shift from extraction to value creation. Expanding downstream processing - across steel, aluminium, fertiliser, and energy - can significantly increase domestic value addition and reduce import dependence. This is particularly true for oil refining, metals processing and phosphorous and nitrogenous fertilizers.

- To get there, infrastructure systems are the enabler of industrialisation at scale. Reliable energy, efficient transport corridors, and market connectivity are not prerequisites alone- they are the platforms through which mineral wealth is converted into industrial capacity.

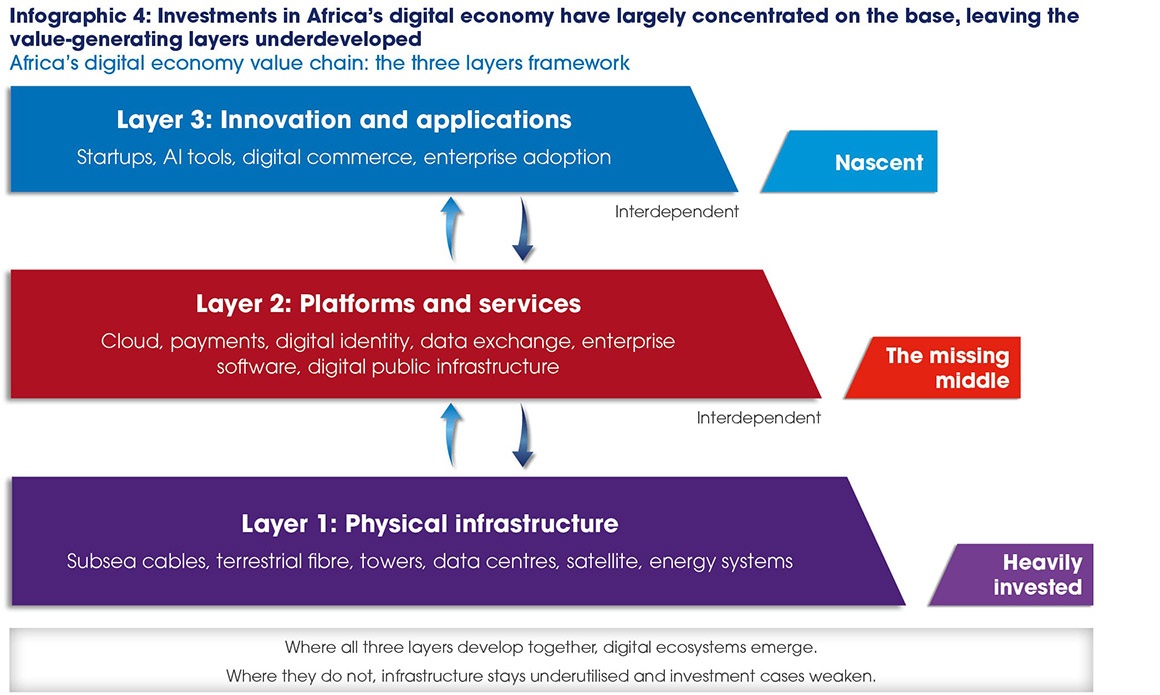

Digital infrastructure

Digital transformation depends on the full stack – international gateways, national backbones, metro networks, data infrastructure, and enterprise platforms functioning together as an integrated system. While Africa has largely solved for international connectivity, the opportunity now lies in building the missing middle to move from infrastructure to economic systems.

- Connectivity alone does not create jobs or productivity. Despite significant increases in bandwidth, the absence of middle- and upper-layer infrastructure means that digital access has not yet translated into proportional gains in industrial activity, services growth, or employment.

- The “missing middle” is the largest investment opportunity. Expanding fibre backbones, cross-border links, Internet Exchange Points, and data centre capacity can unlock domestic traffic, reduce costs, and enable scalable digital businesses.

- Our findings point to a significant upside: countries that successfully convert connectivity into productivity—such as Ghana, where digitally delivered services (DDS) exports reach 6.3% of GDP (on par with India and above the Philippines)—illustrate the scale of opportunity. If Africa’s ten largest economies matched this level, DDS exports could increase from ~$29 billion to ~$127 billion annually, unlocking nearly $100 billion in additional value